Mining

Digital miners

Earn daily BTC rewards effortlessly

Reward calculator

Estimate your potential BTC rewards

GOMINING token

Learn how GOMINING boosts your mining rewards

Miner Wars

Compete and earn BTC and GOMINING

Wallet

Wallet

Buy, send, and receive crypto securely

Crypto cards

Pay with crypto online and in stores

Finance

Simple earn

Earn BTC on your crypto with no lock-ups

Instant Funds

Unlock instant funds by using your assets as collateral.

Launchpad

Access early-stage crypto projects

Travel

Travel

Book hotels & flights worldwide

eSIM

Coming soon

Learn

Academy

Learn crypto step by step for free

Blog & News

Stay updated with insights and trends

Customer help

Find quick answers or contact our support team

Crypto glossary

Key crypto terms explained simply

Benefit programs

GoClub

Exclusive club for GoMiner avatar holders

GoMiners

Own a GoMiner avatar and unlock unique perks

Referral program

Invite friends and earn extra rewards

VIP program

Increase your VIP status and access higher benefits

Company

General

About

What GoMining stands for and how it all started

Careers

Work with a global crypto team

Contacts

For support or partnership inquiries

Tokenomics

GOMINING's structure, utility, and token flow

GoMining reviews

What millions of users say about GoMining

For partners

Advisory board

Experts guiding GoMining's long-term vision

Reports and results

Transparency reports and performance updates

Service providers

Trusted infrastructure partners

Institutional

Institutional-grade Bitcoin mining solutions

GoBTC Pay

AI

Sign up

Log in

Log in

Sign up

EN

Back

News

The Fee Drought: Challenges and Scenarios for Bitcoin’s Mining Future

Aimara García Cabezas

Published:

Sep 18, 2025

·

Edited:

Sep 19, 2025

·

Reading time:

6 min

GoMining News

All news

May 23, 2026

A New Balance Cycle Begins in Miner Wars

May 22, 2026

From Pizza to Sats: Join the Bitcoin Pizza Day Raffle

May 18, 2026

🌋 Magmars Are Live: Fire-Born Avatars With a Blazing Advantage

May 8, 2026

Instant Funds: Access Liquidity Without Letting Go of Your Bitcoin

May 6, 2026

Your AI Speaks GoMining Now: Introducing GoMining MCP Server and AI Skills

May 6, 2026

🌞 Sunny Miami Raffle: Win Exclusive Solar GoBoxes

May 5, 2026

GoMining and Babylon Plan a New Path From BTC Holding to Mining Rewards

You might be interested in:

February 27, 2026

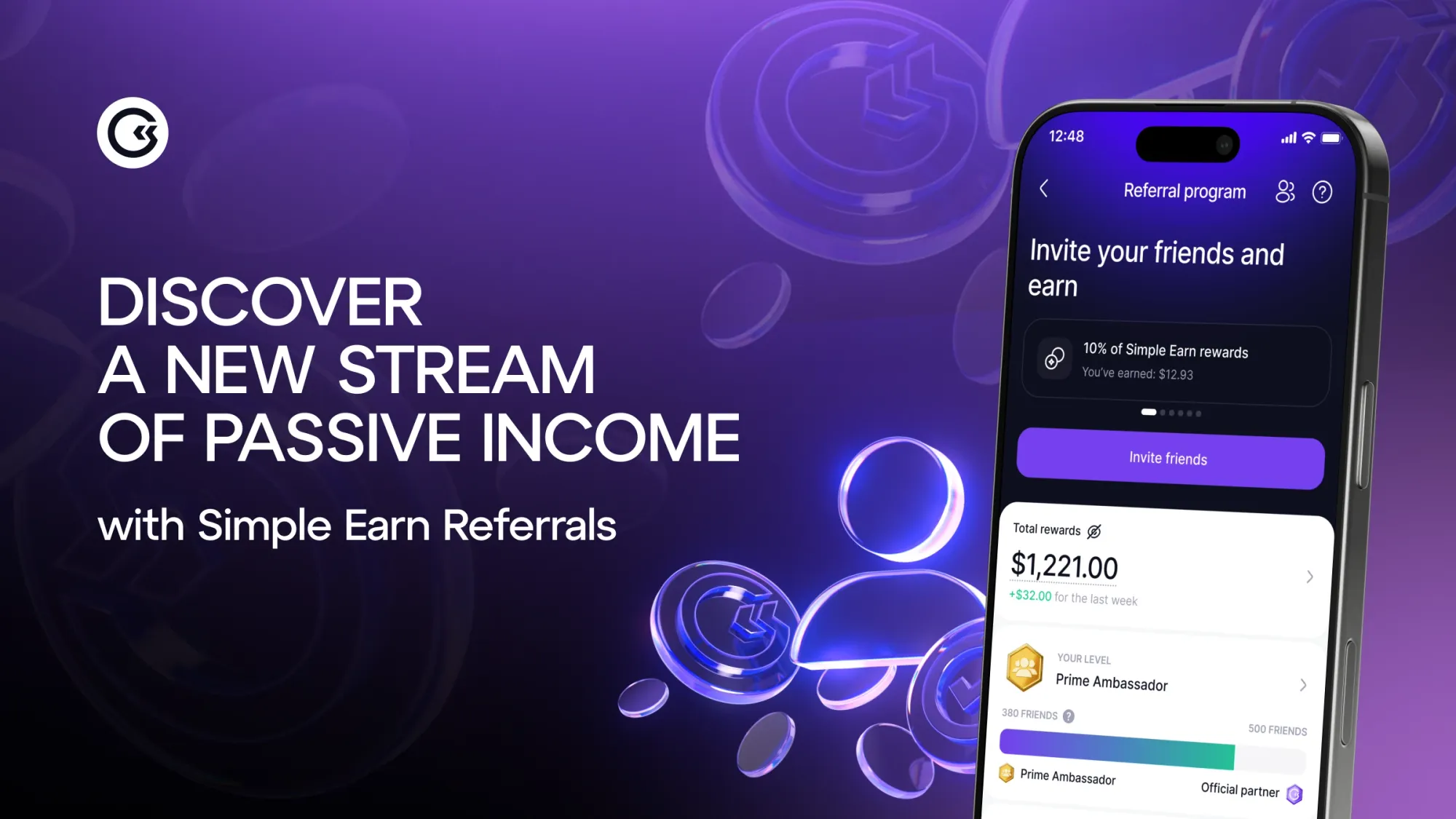

Simple Earn Referrals: Earn 10% of Your Network’s Simple Earn Rewards

April 26, 2026

5 Years of GoMining: From the Mines to the Moon

January 24, 2026

Top 5 Signs Someone is Mining Crypto on Your PC and How to Fix It in 2026

February 26, 2026

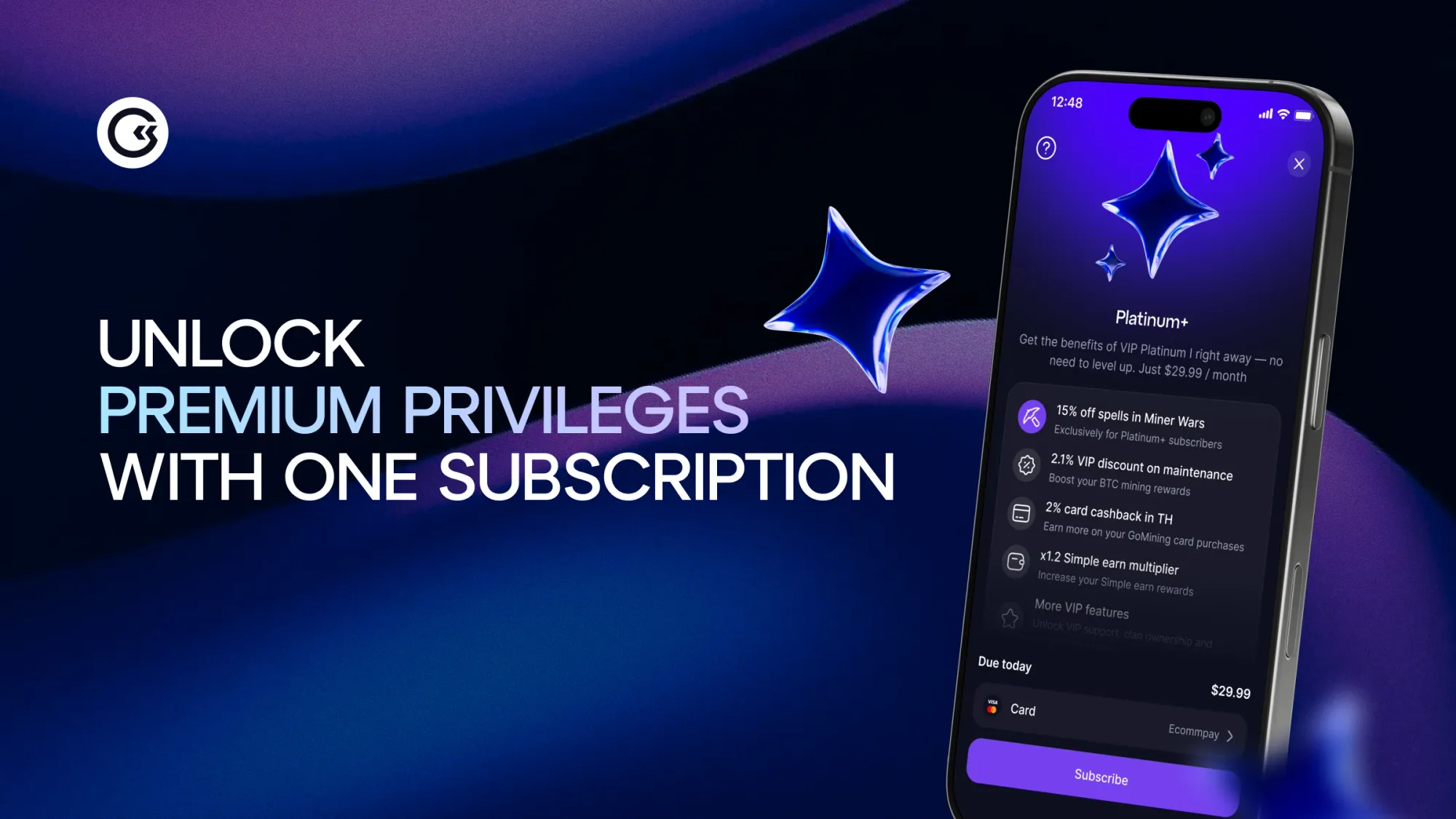

Platinum+ Subscription: Unlock Platinum I VIP Benefits Without Climbing the VIP Ladder