Imagine a typical situation: someone has a regular bank debit card and a bit of cryptocurrency on an exchange or in a wallet. They hear that now you can “connect crypto to a card” and pay with it in a store, and they see the term crypto debit card in the description. This is the moment when most people get confused: the card looks the same, but how exactly does a crypto debit card work?

With a regular debit card, everything is clear: money sits in a bank account, the bank deducts it, the store receives the payment. But what happens if a person taps a terminal with a card that’s not backed by a fiat account, but by a balance in Bitcoin or a stablecoin?

In this article, we’ll break down how a regular debit card differs from a crypto debit card, how they spend money, what advantages and limitations they have, and in which situations one cannot replace the other.

How a Regular Debit Card Works

First, let’s set the foundation. A debit card is a piece of plastic (or a virtual card on your phone) linked to a bank account. That account holds regular money: dollars, euros — or any fiat currency.

Regular debit card

When someone buys a coffee for one dollar, the bank does something very simple: it checks whether there’s enough money. If yes, it reduces the account balance by one dollar, processes the payment through a payment network (like Visa or Mastercard), and the merchant receives one dollar minus the acquiring fee.

The person paying doesn’t see any of this. For them it’s just one gesture — “I tap the card and walk away with my coffee.” But the important detail is this: the source of money is a bank account, and all operations follow the rules of the traditional financial system.

If the bank blocks the card, you can’t pay. If the bank has technical issues, the payment won’t go through. If there’s no money in the account, the terminal declines the transaction.

And another detail: the money on a debit card doesn’t change value on its own. Five thousand dollars added to the account will remain five thousand dollars until it’s spent.

What a Crypto Debit Card Actually Is

Now let’s look at a crypto debit card. Externally, it looks almost identical to a regular card: the same plastic, the same payment network logos, the same option to add it to Apple Pay or Google Pay and pay with your phone.

The main difference isn’t on the surface — it’s inside. The source of funds for such a card is not a bank account, but your crypto balance. It can be funds on an exchange, in a crypto wallet, or in a service that issues the card. That balance can contain Bitcoin, Ethereum, TON, stablecoins like USDT or USDC, and other digital assets.

Crypto debit card

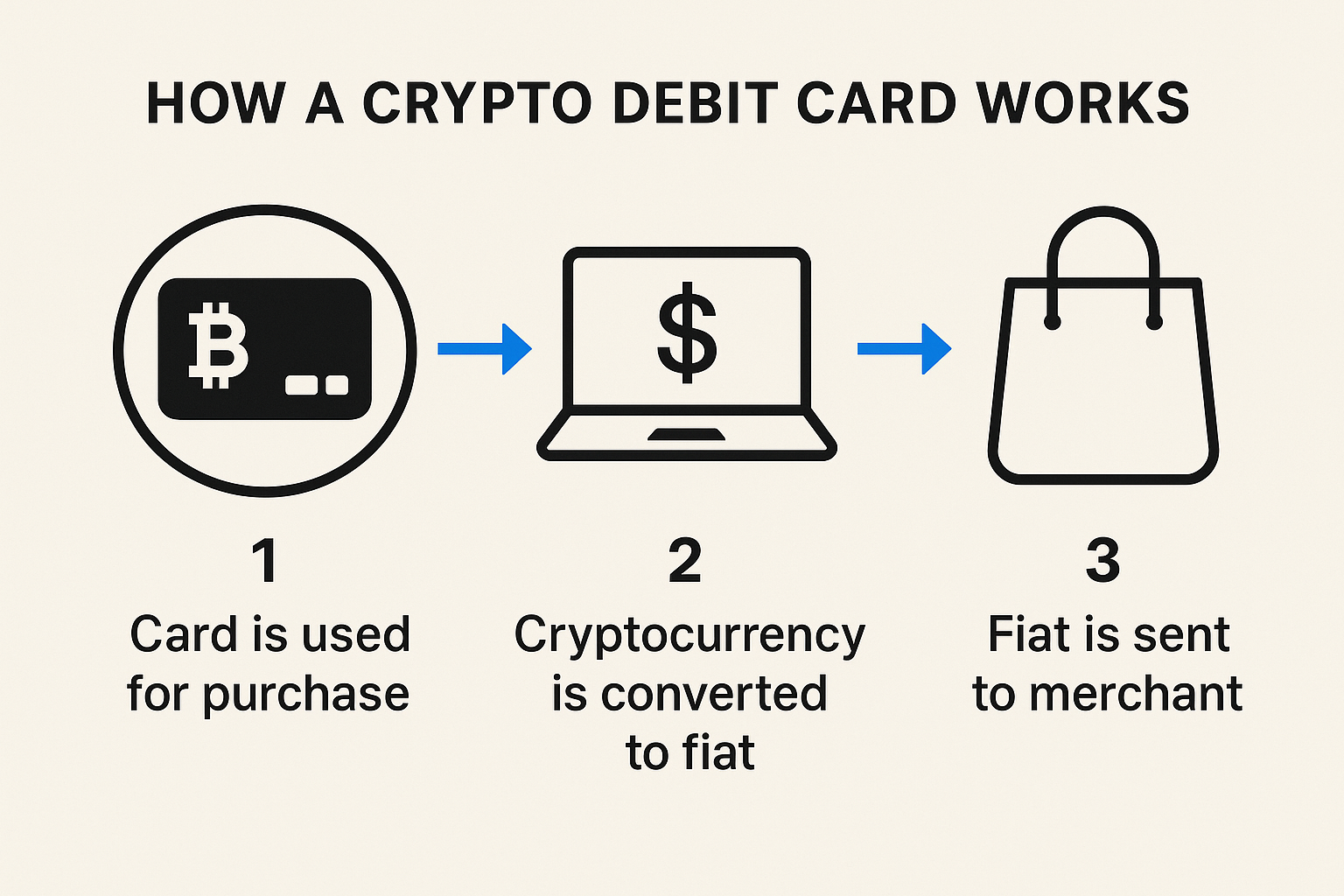

When someone buys a coffee using a crypto debit card, the store still receives regular money in the national currency. The key moment: between tapping the card and the merchant receiving the payment, the service manages to sell a small portion of your crypto at the current market rate and deliver fiat to the seller.

Put simply, Crypto Debit card works like this: You pay with crypto, but the store sees the same payment as from a normal debit card. Behind the scenes the service first sells a bit of your crypto and then sends euros, or dollars to the merchant.

That’s why a crypto debit card is not “a card that sends Bitcoin directly to the store.” It’s a bridge between the crypto world and the regular payment infrastructure, silently converting crypto into fiat with every purchase.

Where the Money Actually Sits

When someone first picks up a crypto card, a natural question appears: “Where is my money actually stored?”

With a regular debit card it’s simple — money is held in a bank on a specific account, and you can see your balance and statements. Everything lives inside the familiar banking system: deposit, spend, check your balance.

How a crypto debit card works

In the case of crypto cards, there are two approaches:For one, the cryptocurrency sits on your exchange balance — for example, on Binance or another major platform. You keep your USDT, BTC, or ETH there, and the card is simply “connected” to this balance. When you pay in a store, the system instantly sells the needed amount of crypto at the current rate, converts it to fiat, and sends it to the merchant. For you, it looks like a normal transaction, but a tiny conversion happens behind the scenes.

In the second approach, your crypto is stored not on an exchange, but in a wallet app connected to the card. The principle is exactly the same: you tap the card, the service automatically sells crypto for the purchase amount, and the store receives regular fiat currency.

In essence, the user lives in two worlds at once. Their money exists in the form of digital assets, but at the moment of payment it turns into euros or dollars — the kind of money any store or Point of Service (POS) terminal understands. Everything happens quickly, so using a crypto card feels the same as using a regular debit card.

Volatility and Stability: Why the Crypto Card Balance Behaves Differently

The key difference between a regular debit card and a crypto debit card is how your balance behaves.

With a normal card, everything is stable: if you have 1,000 euros in your account on Monday and you don’t spend anything, on Friday the balance is still 1,000. 1 euro = 1 euro — the internal balance doesn’t jump around. The euro/dollar exchange rate may move, but your bank balance doesn’t fluctuate because of that.

With a crypto card, it’s like being on a roller coaster. If your balance is stored in Bitcoin, ether, or another volatile coin, the amount in euros or USD or any fiat equivalent can change even when you haven’t spent a cent. Today Bitcoin could be $95,000, tomorrow it could be $155,000 or $65,000. And your card balance moves along with that price.

So a crypto card is both a payment tool and a way to hold an investment. Your money lives its own life: sometimes growing, sometimes falling — even while you’re asleep.

To reduce this “amusement park ride,” many people use stablecoins — digital tokens pegged to the dollar or another fiat currency — for everyday spending. The idea is simple: a stablecoin aims to stay around 1:1 to the dollar, so the card balance becomes more predictable and calm.

But even with stablecoins there are still nuances: service fees, limits, the card issuer’s policies. Total “bank-like stability” still doesn’t exist — but the card’s balance becomes notably more stable.

Fees — Why Paying with a Crypto Card Can Cost More

A regular debit card is built so that most fees are hidden from the user. The merchant pays the bank, the bank shares part of the fee with the payment network, but the cardholder never sees these movements. They only pay in special cases: for example, withdrawing cash or making international transfers.

A crypto card almost always introduces extra layers of cost. When someone buys a product or service, there may be:

- a fee for selling cryptocurrency

- a fee from the service issuing the card

- a network fee if the user previously topped up the balance via blockchain transaction

- a fee for maintaining the card itself

The point isn’t that “a crypto card is always more expensive,” but that fees are part of the business model in finance, including in crypto services, and a new user should read the terms in advance. Sometimes cards offer great rates and low fees to attract customers; sometimes the opposite — conversions may cost noticeably more.

How a crypto debit card works

A good reference point is to compare how much a person gets or spends when exchanging the same amount of crypto via the card versus selling it manually on an exchange and then withdrawing. That quickly shows the markup taken by the service.

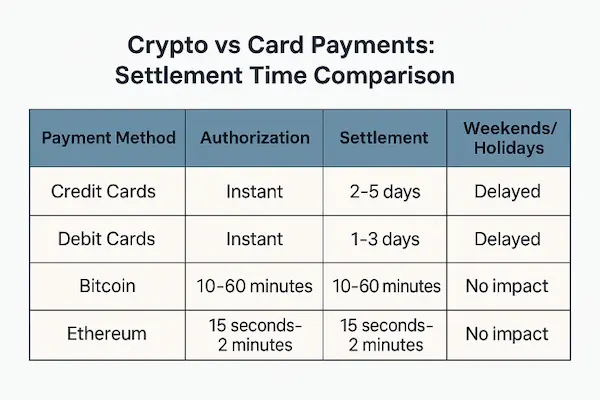

On average, you pay bulky fees from every transaction with a regular card: from 1% and up to 5% per every dollar you send or spend.

These fees look small, but they compound really quickly and can sometimes eat up a substantial amount of money without you realizing it. The lowest amount you can pay for a transaction in crypto is within the 0.01% range. Sure, there’s always the risk of network congestion when price spikes up, but given you can use multiple low-fee blockchains to route the money, you’d be better off than with a regular bank card.

Where Can You Pay With a Crypto Card?

From the merchant’s perspective, a crypto card is indistinguishable from a regular debit card if it’s issued under Visa, Mastercard, or another major payment network. The store has no idea where the money came from — crypto balance or a bank account.

So in theory you can pay with a crypto card anywhere regular cards are accepted: supermarkets, cafés, online stores, streaming subscriptions — everywhere.

In practice, everything depends on local regulations. Some countries treat crypto-linked cards casually. Others impose strict requirements or even ban certain products. Whenever the card issuer faces issues with licensing or its partner bank, using the card can become difficult or impossible.

It’s important to remember that the reliability level of a crypto service and of a traditional bank is still different. Banks have been part of the financial system for decades and insure deposits, while crypto companies operate in a more dynamic environment where rules change much faster.

What It Feels Like for the User

If you forget all the theory and look through the eyes of an ordinary person, a good crypto card should behave “like a regular one.” You link it to an app on your phone and just pay, without thinking about which asset is being sold at that moment.

Often, the app shows the balance directly in fiat equivalent. For example, the account has 0.02 BTC, and next to it, the app displays a number showing how many euros that 0.02 BTC is equal to. A person perceives this as “I have 1,570 euros,” even though what they actually have is Bitcoin that changes in price every day.

The convenience here is that the crypto card lets you spend crypto without going through extra steps like “log in to the exchange → sell → withdraw → wait.”

But that convenience may come with a cost: fees, stricter KYC requirements, or dependence on a particular service.

Security — Risks of Crypto Cards are and what to look out for

With a regular debit card, the main risks for the user are fraud, leaked card data, and temporary blocking due to suspicious activity. Banks have learned to handle these issues fairly well using a mix of SMS codes, push notifications, 3-D Secure, and support lines.

A crypto card adds its own risk layers. If the crypto sits on an exchange, the user must trust the platform to store funds securely and avoid issues like hacks or bankruptcy. History has examples of large exchanges shutting down and clients waiting a long time for refunds.

If the crypto is stored in a personal wallet, a different challenge appears — not losing the seed phrase or private keys. In the crypto world, losing a private key often means irreversible loss of funds.

In addition, any card-connected operations involving crypto may draw more attention from banks and regulators. In some places, they treat it calmly, in others — suspiciously.

For someone new to crypto, it’s useful to start with basic security principles: wallets, seed phrases, key storage. In the Academy you can find dedicated material on how to store cryptocurrency safely and avoid losing access — it fits well alongside the topic of crypto cards.

A Practical Example. One Purchase, Two Approaches

To really feel the difference between a debit card and a crypto card, let’s consider a simple scenario.

A person buys a train ticket for 50 euros. They have a regular debit card with a euro account, and a crypto card with a balance in a dollar-pegged stablecoin.

If they pay with the debit card, the bank deducts 50 euros from the account, the withdrawal shows up in the statement, and that’s it. For them the ticket costs exactly 50 euros — no extra dynamics.

If they pay with the crypto card, the service at the moment of purchase calculates how many dollars in stablecoin are needed to cover 50 euros at the current rate, sells that amount, converts it to euros, and sends the euros to the merchant. There may also be a conversion fee or the service’s markup.

If a week later they check the debit card, they’ll see “500 euros yesterday, now 450.” If they check the crypto card, they’ll see that the crypto balance decreased, and the fiat equivalent might be slightly higher or lower depending on how the market moved during that week.

Same ticket, same “tap and pay” moment — but the flow of money under the hood is completely different.

Who Typically Uses Crypto Cards?

You can say that crypto cards have several common usage scenarios.

First, people who earn or receive part of their income in cryptocurrency. Freelancers, developers, participants of crypto projects. For them, the card is a convenient way to spend crypto on everyday expenses without turning each purchase into a separate exchange transaction.

Second, people who actively invest in crypto assets and don’t want to store large amounts in bank accounts. In this case, the card balance becomes an extension of their investment portfolio. They accept the risk of volatility but gain flexibility: they can hold assets and spend them.

Third, people in countries with strict currency account restrictions. For them, crypto becomes a way to hold value, and the card — a bridge to making payments in stores and online.

At the same time, it’s important to remember: crypto cards do not eliminate the need for a regular bank account. In practice, people keep both tools and choose which one is appropriate for each situation.

Why You Can’t Honestly Claim That One Card Is “Better” Than the Other

The market is full of promotional claims that a crypto card “solves all problems,” “replaces banks,” or “makes payments free.” In reality, things are calmer.

A regular debit card remains the most reliable and predictable tool for daily life. It is tied to a banking system where everything has been polished for decades.

A crypto card adds the ability to spend crypto as conveniently as fiat, but brings volatility, fees, and new risks. For some people, it’s a practical compromise; for others, an unnecessary complication.

A more honest summary would be:

“A regular debit card and a crypto card solve the same problem — allowing you to pay. But each does it in its own way and fits different situations.”

If someone values stability and predictability, they are more comfortable staying on the side of the traditional banking card. If they actively use crypto and want to spend it directly, then it makes sense to understand how a crypto card works, how fees are structured, which providers are reliable, and only then connect such a card.

Bonus: A New Case From Jack Dorsey

Recently, there was news that Square, the payment company owned by Jack Dorsey, launched a new mechanism allowing more than 4 million merchants worldwide to accept payments directly in Bitcoin.

Jack Dorsey

This is an important shift: previously BTC almost always went through conversion into fiat, and now the merchant chooses the format — keep the payment in Bitcoin, automatically convert it to dollars/euros, or mix options (BTC→BTC, BTC→fiat, fiat→BTC, or fiat→fiat).

Receipt paid in BTC

Fees are set to zero until 2027, and then will be 1%, still lower than standard bank card fees. Essentially, Square is turning cryptocurrency from an “exotic” method into a full-fledged payment option suitable for real businesses.

Slowly, but surely, crypto claims its place under the sun with low fees and service payments, at times beating even Visa and Mastercard at cost efficiency of oversea transfers. For instance — remittance payments worldwide are now mostly processed with USDT: it’s around $6 per $100 with bank-to-oversea bank and almost $0.001 fee to send it via blockchain. Maybe one day you won’t have to pick a bank for opening an account, but only a blockchain you’d like to work with.

Summary: What a Beginner Should Know

If we simplify the whole topic into everyday language, the difference between a regular debit card and a crypto debit card boils down to the source of money and how that money behaves.

A regular card is stable and straightforward: the account holds euros or dollars, they retain their value, and spending has no surprises. A crypto card holds cryptocurrency, and each purchase converts a bit of that crypto into fiat at the moment of payment.

So using a crypto card feels almost as easy as using a bank card, but under the hood there is always a tiny exchange operation. The balance can rise or fall with the market; fees depend on the service; and risks range from volatility to the reliability of the platform that stores your assets.

But if someone already owns crypto and wants to spend it directly, a crypto card becomes a convenient bridge between digital assets and ordinary life. The main thing is to understand how it works, not expect “magic,” and use it in situations where it genuinely helps.

To start from the basics, check out the free GoMining Academy Course on Crypto and Bitcoin Mining from Scratch at 👉 GoMining

Telegram | Discord | Twitter (X) | Medium | Instagram

FAQ

What is the main difference between a regular debit card and a crypto debit card?A regular card spends money from a bank account. A crypto card spends your cryptocurrency by automatically selling it at the moment of payment and sending fiat to the merchant.

Does the merchant receive cryptocurrency?No. The merchant always receives regular money — euros, dollars, yen etc. The crypto-to-fiat conversion happens inside the service that issued the card.

Is cryptocurrency stored on the card itself?No. It’s stored either on your exchange balance or in the wallet of the service connected to the card. The card simply provides access to those funds.

Do you still need a bank if you have a crypto debit card?Yes. The card works through payment networks like Visa or Mastercard, and these networks interact with banks. The only difference is where the money for the payment comes from.

What happens if the price of cryptocurrency drops sharply?The balance of the crypto card decreases in fiat terms even if you didn’t make any purchases. That’s normal — crypto changes in value, and the card reflects that.

Can you use a crypto card in any country?Technically, yes — the terminal can’t tell the difference. But restrictions may appear due to local regulations or restrictions from the card issuer.

Are there fees?Most of the time, yes. The main costs are crypto conversion at the moment of payment, service fees, and possible network fees when topping up.

Is a crypto debit card safe?It’s as safe as the issuer service and the place where your crypto is stored. The risks differ from a regular card: exchanges can shut down, and private keys can be lost.

Can you keep stablecoins on a crypto card to avoid price fluctuations?Yes. This is common practice: USDT, USDC, and other stablecoins make the balance more predictable, similar to a regular bank account.

Does a crypto debit card replace a bank card?Generally speaking, no. It’s an additional tool. It’s useful if you hold crypto and want to spend it directly in everyday stores. However, a bank card can still be needed for building credit and accessing other traditional banking services.