Read this article to understand how tokenization works, what it is, what risks it has and how it makes your life easier.

Imagine owning a gold bar, a small share of an apartment, a couple of government bonds, or even a digital asset like stETH. All of that has real value, but dealing with these things in the traditional world is a hassle: gold needs to be stored, real estate requires paperwork, bonds are bought through brokers, and none of these assets can be moved or managed instantly.

Tokenized assets solve this problem. Tokenization lets you “package” real or digital value into a token on a blockchain. This token isn’t just a pretty picture — it represents your legal right to a specific asset: gold in a vault, a fraction of a property, a bond, a commodity, a share of a fund — or even an existing crypto instrument such as a staked token.

On the surface, everything looks simple: take a real asset, create a token representing it, and move it into Web3. But behind this simplicity stands a large infrastructure — custodians who hold real assets, legal frameworks, regulation, reserve audits, price oracles, and smart contracts that ensure the system works transparently and fairly.

Tokenization offers several powerful benefits: 24/7 access, the ability to own tiny fractions of assets, full transparency of all movements, and seamless integration with DeFi. At the same time, tokenized assets also come with risks — dependence on custodians, regulatory constraints, the accuracy of price oracles, and the quality of the redemption mechanism that allows you to convert the token back into the real asset.

Simple Explanation of how Tokenization Works

A tokenized asset is simply a digital token that confirms ownership of something real. Essentially, it’s a digital document that states: you own a specific asset held by a trusted custodian. Blockchain only changes the format — it moves ownership into a digital environment where transfers and accounting become easier and more accessible. Much like stock allows you to hold a small piece of a company, tokenized assets make it easier to transfer value, but they’re not limited to only one company and are much easier to send, store, receive and exchange.

Unique collections from Gomining

Types of Tokenized Assets

1. Real-World Assets (RWA)

This is the fastest-growing segment because it bridges traditional finance and Web3. Think of the old financial world — gold, bonds, oil, real estate — existing in its own closed ecosystem, while Web3 lived separately. In 2025, these worlds finally started merging. That’s why RWAs became the biggest trend of the year. Giants like BlackRock, Tether, Franklin Templeton, Fidelity, Coinbase, and Circle are entering the space because users want real assets in a blockchain-friendly form.

Tokenized U.S. Treasury Bills. These are real treasury bonds held by a custodian, while you own a token referencing them. They’re popular because they offer stable 4–5% yields and are considered a safe asset. Notable projects: Ondo Finance, Backed Finance.

Tokenized Real Estate. You can buy a tiny share of a real property — even 0.1% of a building or apartment. It lowers the barrier to entering the real-estate market, which is normally expensive and slow. Example: Realt.

Tokenized Gold. 1 PAXG token = 1 troy ounce of physical gold stored in a London vault. It’s like owning gold without keeping bars under your bed. Example: PAX Gold (PAXG).

Tokenized Commodities. Even oil or silver can be tokenized — a useful tool for traders and DeFi protocols looking for real-asset exposure.Examples: Tiberius (metals), Kinesis Silver (KSILV).

Tokenized Corporate Bonds. A company’s debt packaged into a token. Works like normal bonds but faster and cheaper to handle. Example: Backed Finance issues tokens referencing Apple and Tesla corporate debt.

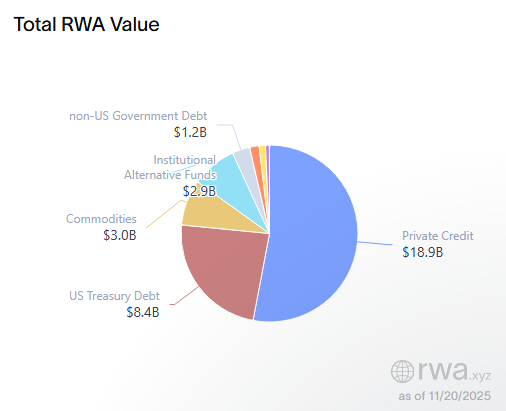

Where to track RWA statistics? The easiest dashboard is RWA.xyz — a simple real-time overview of total tokenized asset volume, top issuers, and market momentum.

Source: app.rwa.xyz

2. Digital-Native Assets (digital-native tokens)

These are assets that originate inside blockchain ecosystems — they have no physical equivalent. They act like “virtual versions” of existing crypto or financial tools, designed for flexibility, interoperability, and new functions inside Web3.

Wrapped Tokens (e.g., WBTC). Imagine you have BTC but want to use it in DeFi — lend it, trade it, or farm with it. Bitcoin can’t do this on its own network, so it gets “wrapped” into a token and moved to Ethereum. The result is a digital twin of Bitcoin, equal in price but able to function where Bitcoin itself can’t.Example: WBTC — Wrapped Bitcoin.

Liquid Staking Tokens (LST), such as stETH. When you stake ETH, you can receive a token proving your ETH is locked in staking and earning rewards. This token can be traded, used in DeFi, or sent to someone else while your original ETH keeps working as a validator.Example: stETH by Lido.

Synthetic / Derivative Tokens (on-chain derivatives). Tokens created on a blockchain to mirror the price or yield of other crypto assets. Examples: sETH, sUSD, sBTC (Synthetix ecosystem).

Why this category stands alone? Because these assets: — have no physical backing, — are created directly on-chain, — exist to support Web3 functions, — help crypto assets move across networks and gain new utilities.

They act like adapters and containers in the Web3 world, making the system more flexible and liquid.

3. Tokenized Funds and Securities

In simple terms, tokenized funds are the same ETFs, mutual fund shares, or company stakes — just in a more convenient digital form.

Imagine a typical index fund like S&P 500 or Nasdaq-ETF. In TradFi, you need a broker, a lot of paperwork, access to a stock exchange, and you’re limited to trading hours. Tokenization removes these barriers: the fund exists as a blockchain token, stored in your wallet, transferable in seconds, and tradable 24/7. Leading examples:

Franklin Templeton — Franklin OnChain U.S. Government Fund (FOBXX). One of the world’s largest asset managers tokenized part of their government bond fund on Stellar and Polygon — the first registered fund to operate fully on-chain.Website: https://www.franklintempleton.com

BlackRock — BUIDL Tokenized Fund. The largest asset manager on Earth ($10T+) entered tokenization with BUIDL, a fully on-chain fund backed by U.S. treasuries.Website: https://blackrock.com

Ondo Finance — OUSG. A tokenized version of BlackRock’s U.S. treasuries fund.Website: https://ondo.finance

WisdomTree Prime. A major ETF issuer with a full line of tokenized funds in the U.S. Website: https://www.wisdomtreeprime.com

4. Stablecoins as a form of tokenization

Stablecoins are actually tokenized too — they are tokenized dollars. Imagine a digital banknote. You hold a token like USDT or USDC, while real dollars, Treasury bills, and other safe assets sit with a custodian. The token is like a digital receipt saying: “This token is backed by 1 real dollar.”

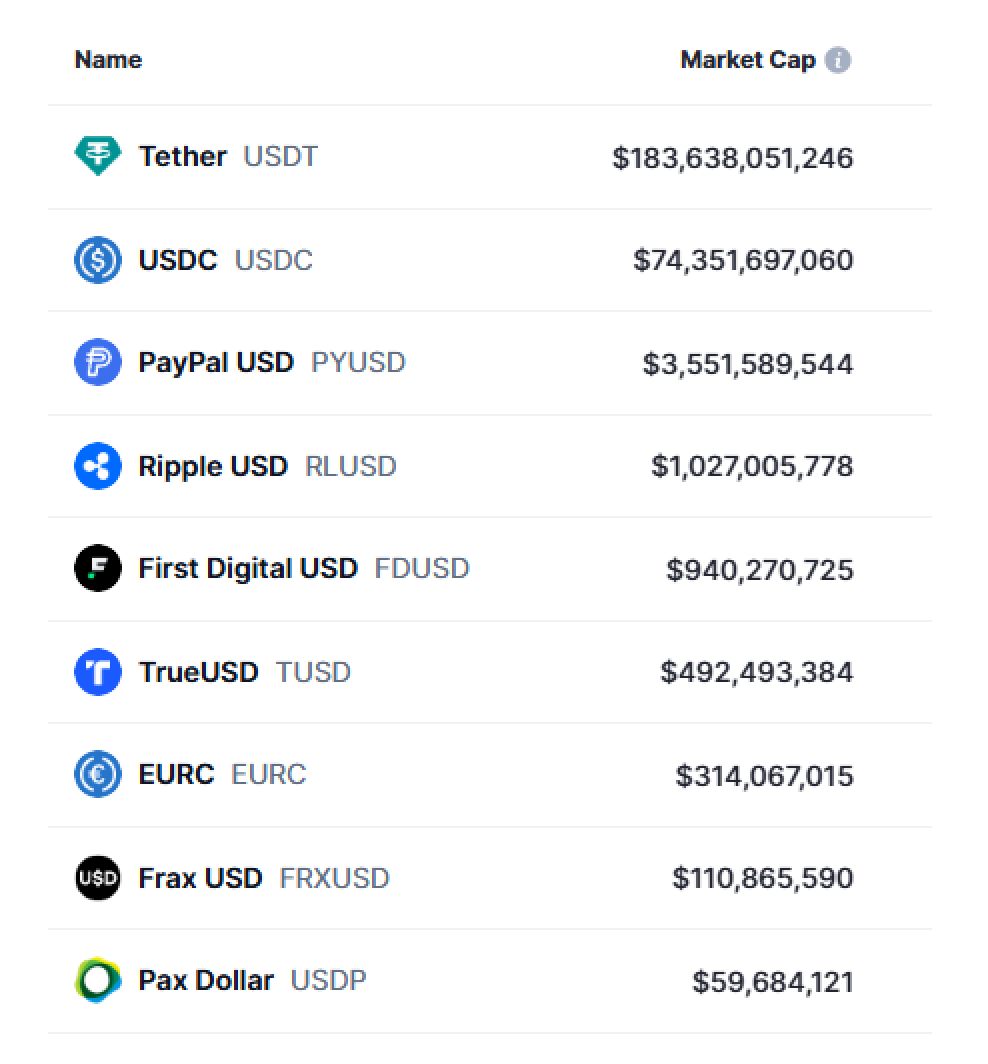

Largest stablecoins by market capitalization

Stablecoins work so massively because they’re the most convenient instrument in crypto: available 24/7, transferred in seconds, transparent (you can see flows on-chain), and integrated into every DeFi platform. Top projects:

USDT (Tether) — the largest stablecoin with $180B+ in circulation. Backed by Treasuries, banks, liquid instruments. In 2025, Tether expanded into RWA, tokenizing Treasuries and other commercial assets.Website — https://tether.to

USDC (Circle) — the second largest stablecoin and the most regulation-friendly. Supported by major banks and auditors; compatible with Apple Pay and financial rails. Circle also issues tokenized Treasuries via Reserve Funds.Website — https://www.circle.com

PYUSD (PayPal) — a major step in bringing tokenized currency to mainstream U.S. users. Website — https://paypal.com

EUROe — a European fully-backed digital euro.

GUSD (Gemini) — a fully regulated stablecoin issued by Gemini.

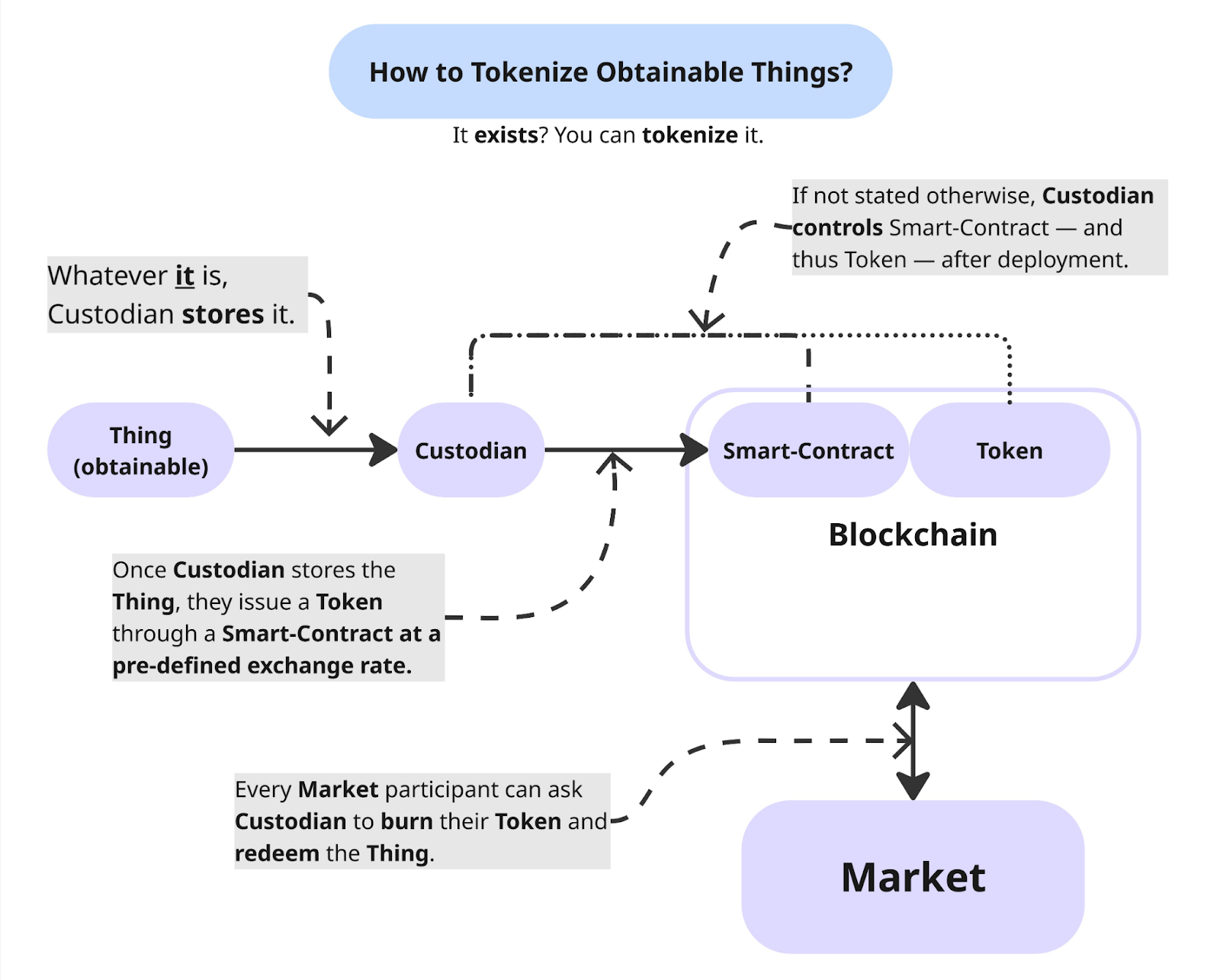

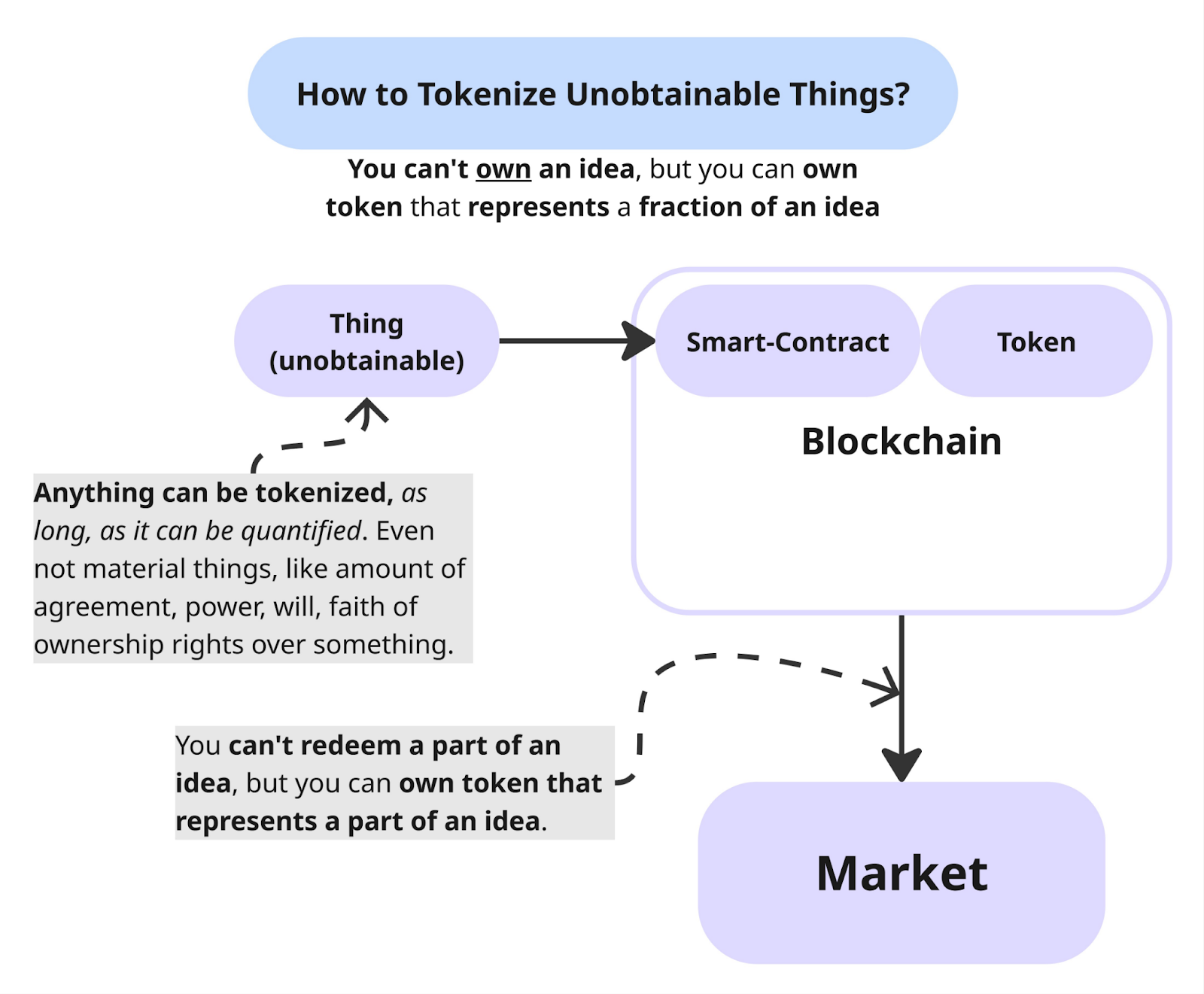

How tokenization works

Tokenization looks elegant from the outside: you take gold, bonds, or real estate and turn it into a convenient digital token. But behind the scenes, the process is very structured and grounded.

Explanation of idea tokenization, such as with memecoins

Imagine shipping a parcel: you must describe what you’re sending, where it’s stored, who’s responsible, how it’s verified, and how the recipient can pick it up. Tokenization follows the same logic — only in a financial environment.

First, the asset is “digitized.”A company or platform defines which asset backs the token — gold, bonds, real estate, or something else. Then they document the basics: where the asset is stored, who is responsible for it, how its existence is proven, and which rights the token holder receives (ownership, yield, redemption, etc.). It’s like creating a product listing before putting it on an online marketplace.

Then the asset is placed under custody and regulation.The physical object — gold, securities, property certificates — is stored with a licensed custodian: a bank, trust, or digital depository. Without real custody, the token becomes nothing more than a nice picture. So KYC checks, AML requirements, audits, and reporting come into play. This is what builds trust from the TradFi world.

Next comes token issuance on a blockchain.Once everything is clear with the asset, a token is issued on a network like Ethereum, Solana, or Polygon. The smart contract defines how many tokens will exist, who can transfer them, who can run upgrades, and how they can be redeemed for the real asset. The contract works as a rulebook that cannot be changed retroactively.

Then oracles and proofs-of-reserves step in.To ensure the token reflects the real asset’s value, oracles like Chainlink feed updated prices for gold, the dollar, bonds, or real estate. Proof-of-reserves provides public evidence that the asset exists in the right place and right amount — like online receipts confirming everything is where it should be.

Finally, the token can be redeemed.If needed, the user can return the token and receive the real asset or money. The process varies: some projects let you withdraw dollars, others let you redeem gold or realize the bond’s payout. It all depends on the asset and the regulatory setup.

Asset tokenization scheme

Advantages of tokenization

The biggest strength of tokenization is that it makes working with real assets as simple as sending USDT.

24/7 liquidity. Traditional markets follow strict hours: when the exchange closes, you wait for the next day. With tokens, blockchain never sleeps — you can buy, sell, or transfer anytime, including holidays and nights.

Fractional ownership. You don’t need to buy a full gold bar or an entire property — you can own a tiny fraction, like 0.005 ounces or 0.1% of a building. This lowers the entry barrier and opens markets to people with smaller budgets.

Transparency. Everything is visible on-chain: token movements, total supply, confirmed reserves. No need to trust anyone’s word — everything is verifiable.

Fast settlement. Traditional transfers of ownership may take days or weeks due to lawyers, depositories, and checks. With tokens, the transaction settles within seconds.

DeFi integration. A token can be used as collateral, traded, or yield-farmed — it becomes a living part of the ecosystem, not just a paper entry.

Read also: Why it's worth storing some of your assets in cryptocurrency.

Risks and limitations of tokenization

Tokenization also carries risks. It’s important to understand them.

Custodian risk. Even if the token is perfect, a real asset must exist behind it.If the bank or trust storing the assets collapses or gets sanctioned, access to the backing can be lost.

Regulation. Many tokenized assets count as securities—meaning KYC, reporting, and regulatory oversight. Sometimes access is limited for regular users.

Oracles. If an oracle fails or provides incorrect data, the token may show the wrong price, causing issues in DeFi.

Redemption limits. Not all tokens can be redeemed easily. Some require accredited investor status, some take time, and some cap the amount.

Liquidity fragmentation. Tokens issued across multiple networks (Ethereum, Solana, Polygon) split liquidity between platforms.

How to evaluate a tokenized asset

Before trusting a tokenized asset, treat it like a seller on a marketplace. You want to know who’s behind it, whether their claims are real, and what happens if you need a refund.

1. Who is the custodian? The core question. A reliable custodian is like buying electronics from an official store. A shady one is like ordering an iPhone from a seller with no reviews.

2. Are there public proof-of-reserves? These are the “receipts” confirming the asset exists. Strong projects publish audits, reports, and API data.

3. How is NAV calculated? NAV shows the real value behind the token. If the project explains its method clearly and updates often — good. If the math is vague — you don’t know what you’re buying.

4. Is redemption available, and to whom? Redemption is your ability to swap the token back for the asset or cash. Sometimes it’s open to all users; sometimes only big investors.If redemption doesn’t exist at all, the token becomes a “sealed jar” — you can hold it but can’t access what’s inside.

5. Which chain does it run on? Ethereum, Solana, Polygon, Avalanche, or a private network. This affects fees, speed, and DeFi compatibility.

6. Is it legally a security? If so, KYC and reporting apply. Not necessarily bad — just important to know where you stand.

7. Are there regular audits? Good projects always undergo external audits.

The ideal picture: everything is clear, transparent, and backed by documentation.

The future of tokenization

Tokenization isn’t a temporary hype — it’s a major technological shift. We’re roughly where the internet was in the early 2000s: people are only starting to grasp the size of this market.

1. Bonds and government securities will move fully on-chain

Governments and big asset managers have no reason to keep outdated registries. Tokens make settlement faster, cheaper, and more transparent. In the coming years, trillions of dollars in bonds will live on blockchain rails.

2. Access to commodities and real estate will become easier

Buying a piece of commercial real estate or a portion of a gold bar used to be almost impossible. Now it takes a few clicks — and you own a share, just like a stock. Tokenization removes the biggest barrier: high entry cost.

3. Web3 will receive massive institutional capital inflows

BlackRock, Fidelity, Franklin Templeton, Tether, Circle — they’re already here. When giants enter a market, capital follows.

4. DeFi will finally connect with the real economy

Instead of recycling internal tokens, DeFi will work with real assets — Treasuries, real estate, gold, commodities, corporate debt. It’s like crypto exchanges suddenly gaining access to real financial instruments, not just digital abstractions.

Summary

Tokenization is essentially a new transport system for the old world of finance.

For decades, real assets lived in closed, isolated systems: bonds with brokers, real estate with notaries, gold in vaults, commodities on regulated exchanges — each with its own rules and intermediaries. Web3 introduced another way to move value: instant, global, transparent, and without unnecessary friction.

Tokenization is the bridge between these two worlds.The bridge is already operational — and the first “cars” are driving across it: tokenized U.S. treasuries, PAXG gold, Backed Finance securities, RealT property, and stablecoins from Circle and Tether.

In the next 3–5 years, more real assets will cross this bridge: bonds, commodities, real estate, corporate debt, and eventually entire financial products.

For users, this means simpler access, fewer intermediaries, less bureaucracy, and far more choice. We’re witnessing the shift from paper-based finance to digital-native finance — just like the evolution from button phones to smartphones. And there’s no turning back.

Sign up and get access to free (for now) GoMining course on crypto and Bitcoin mining.

Telegram | Discord | Twitter (X) | Medium | Instagram

FAQ

1. What exactly is a tokenized asset? A digital token backed by a real asset: gold, bonds, real estate, commodities, or a financial instrument in Web3.

2. Is it a cryptocurrency? No. It’s not a speculative token — it’s a digital receipt proving ownership of a real asset.

3. Where is the underlying asset stored? In a bank, trust, or licensed custodian, which holds legal responsibility.

4. Why use tokens if traditional markets already exist? Tokens enable instant transfers, 24/7 access, fractional ownership, and reduced reliance on intermediaries — something TradFi doesn't offer.

5. Can you own a tiny piece of an asset? Yes. Even 0.1% of a property or 0.005 oz of gold — that’s the whole point.

6. How do you verify the asset is real? Through proof-of-reserves, audits, and custodian reports.

7. Can the token be redeemed for the actual asset? Yes — if the project supports redemption. Some let you withdraw gold; others return dollars.

8. Are there risks? Yes. The main ones are custodian reliability, regulation, oracle accuracy, and redemption availability.

9. How is this different from stablecoins? Stablecoins tokenize currency (USD).RWA tokenize everything else — bonds, commodities, property, funds.

10. Why is 2025 explosive for RWA? Because institutions like BlackRock, Franklin Templeton, Tether, Fidelity, and Circle have moved into tokenization and are shifting trillions into digital formats.