Recovery Returns as Mining Conditions Begin to Stabilise

March marked the first real pause in Bitcoin’s 2026 drawdown. After five consecutive losing months, BTC closed modestly higher and briefly pushed back above $75,000 before fading into quarter-end. At the same time, institutional demand started to reappear. U.S. spot Bitcoin ETFs returned to net inflows, Strategy continued adding to its treasury, and the network crossed the 20 million BTC milestone.

Beneath that relative resilience, however, mining economics remained compressed. Difficulty fell sharply in March, hashprice recovered from post-halving lows, and the gap between efficient operators and weaker miners continued to widen. Rather than signalling a clean recovery, March looked more like a stabilisation month where accumulation returned, with early signs of relief emerging on the supply side.

TLDR;

BTC: $68,234.92 ▲ 1.4

%Open: $67,291.01 | Close: $68,234.92 | High: $75,000 | Low: $64,500

Hashprice: $32.15/PH/day ▲ 10.2

%Open: $29.18 PH/day | Close: $32.15 PH/day | High: $33.00 PH/day | Low: $28.50 PH/day

Hashrate: 1,021 EH/s ▼ 6.0

%Open: 1,086 EH/s | Close: 1,021 EH/s | High: 1,100 EH/s | Low: 1,010 EH/s

Bitcoin Snaps Its Losing Streak

March was not a breakout month, but it was an important stabilisation month. Bitcoin opened at $67,291.01, rallied strongly into the middle of the month, briefly trading above $75,000, and then gave back part of that move before still closing the month modestly positive at $68,234.92. That matters because it marked Bitcoin’s first positive monthly close in five months, suggesting that the forced unwind phase that dominated the start of 2026 may finally be easing, even if conviction is not yet fully back.

What March showed is that Bitcoin can still attract buyers into weakness, but it remains highly sensitive to positioning and broader risk sentiment. The move higher was strong enough to break the losing streak, but not yet strong enough to confirm that a broader trend reversal is underway. For now, the market looks more stabilised than fully repaired.

Source: Coinglass, Bitcoin monthly returns data

ETF Flows Turn Positive Again

The clearest sign of improving institutional sentiment came from the ETF complex. U.S. spot Bitcoin ETFs recorded $1.32 billion in net inflows in March, ending a four-month streak of outflows and posting their first positive month since October 2025. That rebound came as Bitcoin stabilised above the $65,000 level, suggesting institutions have started treating this range as an accumulation zone rather than a reason to keep de-risking.

That shift should not be overstated. ETF flows are still below the pace seen during the strongest parts of the 2025 cycle, and broader demand remains selective. But after months of persistent withdrawals, March was the first month in a while where the institutional tape started to look constructive again.

Bitcoin Enters the Final Million Era

March also delivered one of the most symbolic milestones in Bitcoin’s history. On March 9, the network crossed 20 million BTC mined, meaning more than 95% of Bitcoin’s fixed 21 million supply is now already in circulation. The remaining one million coins will take roughly another 114 years to be issued.

This milestone does not change near-term price action overnight, but it sharpens one of Bitcoin’s core investment properties: absolute scarcity. At a time when access continues to improve through ETFs, public vehicles, and institutional platforms, that supply backdrop remains one of the strongest long-term pillars supporting the asset.

Strategy Keeps Accumulating Through the Volatility

March also reinforced the point that the largest conviction buyers are not waiting for perfect conditions. Strategy disclosed on March 23 that it held 762,099 BTC after adding 1,031 BTC that week, and market reporting noted that the company invested about $1.66 billion in Q1 2026 to purchase 41,362 BTC overall.

Whatever one thinks of the capital structure behind it, the message to the market is clear: the largest corporate treasury buyer continues to use volatility as an opportunity to increase exposure, not reduce it.

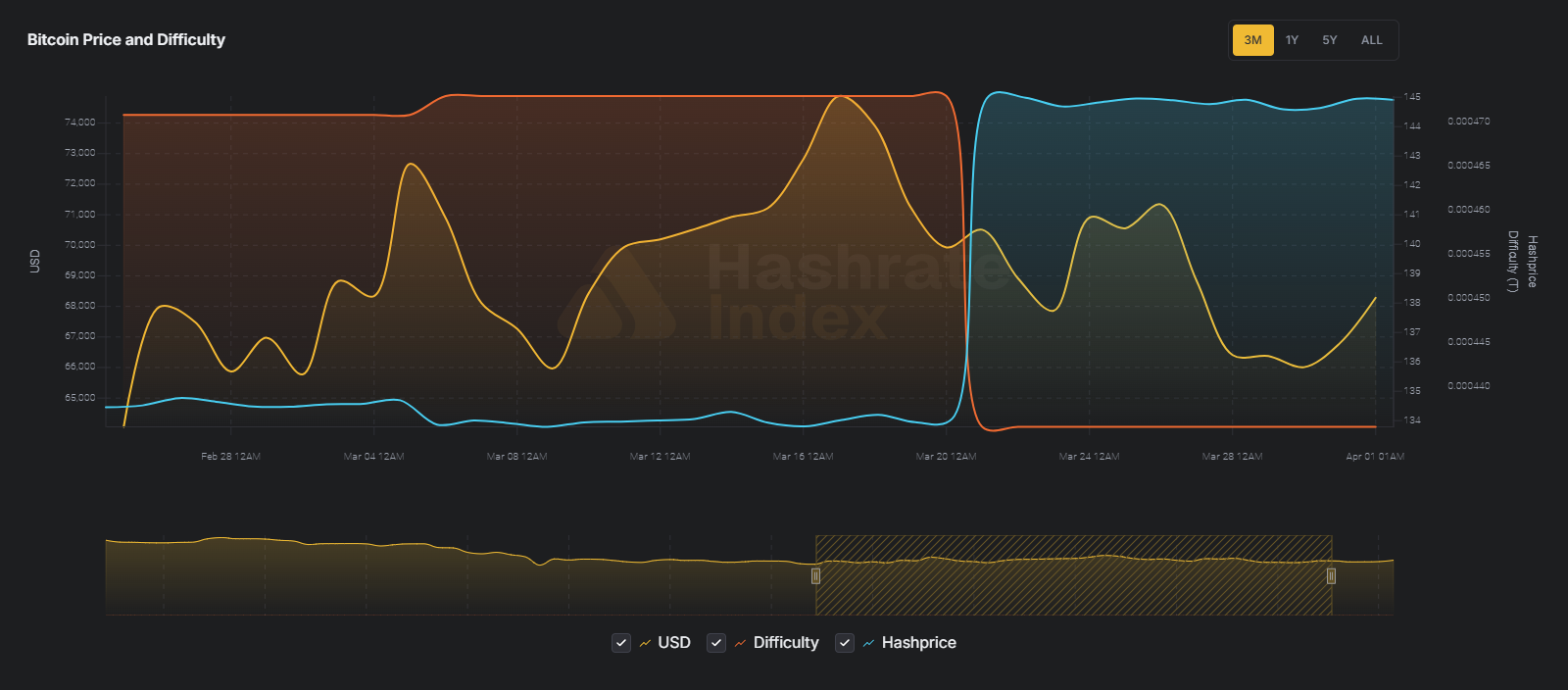

Difficulty Drops as Miner Stress Eases Slightly

On the mining side, March showed how tight the network’s economics remain, but also where conditions began to stabilize. Bitcoin difficulty fell 7.76% on March 20 to 133.79T, one of the sharpest downward adjustments of the year and a clear signal that meaningful hashpower had been forced offline.

At the same time, March closed with a hashrate lower than where it began, while hashprice recovered 10.2% month on month from a deeply depressed base. That combination tells an important story: conditions improved modestly, as reduced competition began to support miner economics.

Source: Hashrate Index, Bitcoin network data, March 2026

The Miner Squeeze Is Creating a Wider Strategic Divide

CoinShares’ Q1 2026 mining report makes the broader picture clear. Hashprice in Q1 fell to around $29/PH/s/day, roughly 15% to 20% of the global fleet was estimated to be unprofitable, and over $70 billion in cumulative AI and HPC contracts had already been announced across the listed mining sector. WULF, CORZ, CIFR, and HUT are increasingly being valued not simply as miners, but as data centre businesses with Bitcoin exposure.

This is becoming one of the defining themes of the cycle. The sector is no longer just being sorted by hashrate growth or machine efficiency. It is being sorted by capital discipline, balance-sheet resilience, and strategic optionality. In that sense, March reinforced a hard truth: even with early signs of relief, mining remains a test of who can survive, adapt, and still fund the next phase of growth.

March did not deliver euphoria, but it did deliver something arguably more important: evidence that Bitcoin can stabilize, attract fresh institutional inflows, and strengthen its scarcity narrative while early signs of relief begin to emerge on the supply side. If ETF demand continues to recover and macro conditions become less hostile, March may end up being remembered as the month the market started to rebuild. But unless price meaningfully re-rates higher, miners will remain in a challenging post-halving environment.